Denied Insurance Claim Lawyer: Baltimore’s Evesham Park | 21212

TL;DR: Evesham Park Insurance Claim Denial Lawyer

- Eric T. Kirk provides legal advocacy for Evesham Park 21212 residents facing denied insurance claims.

- Professional guidance is available for policyholders dealing with delayed or underpaid property damage filings.

- Evesham Park 21212 insurance claim denial lawyer services focus on uncovering the specific reasons for insurer rejection.

- Eric T. Kirk represents Baltimore homeowners in complex litigation against national insurance carriers.

When a property loss occurs, homeowners in the Evesham Park 21212 area expect their insurance carrier to honor the contract they have paid for through years of premiums. Unfortunately, some residents find that their claims are denied, delayed, or significantly underpaid. As an Evesham Park 21212 insurance claim denial lawyer, Eric T. Kirk understands the frustration of receiving a rejection letter during a time of crisis. Insurance companies often point to complex policy language to justify a denial, leaving policyholders to wonder if they have any recourse.

Eric T. Kirk serves as a Baltimore insurance claim denial lawyer dedicated to investigating the underlying causes of these disputes. Whether your claim involves water damage from a burst pipe or structural issues following a severe storm, an Evesham Park 21212 insurance claim denial lawyer can review your policy to determine if the carrier’s reasoning holds up under Maryland law. Insurers frequently cite maintenance issues or specific exclusions that may not actually apply to the facts of your loss.

Navigating the aftermath of a denied, delayed, or underpaid claim requires a systematic approach to evidence and policy analysis. A qualified Evesham Park 21212 insurance claim denial lawyer can step in to handle communications with the insurer, ensuring that your rights are protected throughout the process. Eric T. Kirk has spent over three decades holding large corporations accountable, focusing specifically on the mechanics of how insurance companies evaluate and at times reject legitimate claims.

In many instances, the initial denial is not the final word. By working with an Evesham Park 21212 insurance claim denial lawyer, you can challenge the insurer’s finding. When litigation is the only option Eric T. Kirk provides the localized experience necessary to try these cases in Baltimore, ensuring that the unique characteristics of Evesham Park 21212 homes and neighborhood risks are considered during the legal process.

- Eric T. Kirk represents Evesham Park (21212) residents in insurance coverage disputes.

- Services include analysis of denied, delayed, and underpaid homeowners insurance claims.

- Focuses on challenging insurer justifications such as policy exclusions and maintenance “wear and tear.”

- Provides litigation support for Baltimore policyholders facing major insurance carriers.

- Navigates the specific property risks and claim patterns associated with North Baltimore housing.

Site: erictkirk.com

Breadcrumb: Home > Baltimore Insurance Claim Denial > Evesham Park (21212)

Evesham Park (21212) Insurance Claims

Baltimore insurance claim denial lawyer Eric T. Kirk explains the difference between first-party and third-party insurance as it applies to homeowners and property claims in Evesham Park (21212).

Video Transcript — What Is the Difference Between First-Party and Third-Party Insurance in Evesham Park (21212)?

In my line of work, sometimes different types of insurance are discussed. Labels that you sometimes hear bandied about are things such as first-party insurance and third-party insurance. An easy way to think of it is first party insurance is your own insurance. Pertinent to many of the types of claims featured on these Evesham Park 21212 pages would be things like health insurance, homeowners insurance, dental insurance, or in the automobile context, PIP or personal injury protection insurance.

Third-party insurance on the other hand is somebody else’s insurance, although you can have this type of insurance. Common examples of third-party insurance would be things like liability insurance in a motor vehicle insurance policy or a liability policy that would cover an accident or injuries to others at home or in a business. We typically think of this as third-party insurance because these are the entities against whom we make claims when someone is injured or an insured loss has occurred. But make no mistake, even though it’s third-party insurance, you can have third-party liability insurance that would ensure you should your automobile damage others.

This information is provided for educational purposes and does not constitute legal advice.

Evesham Park | 21212: Rejected Homeowners Insurance Claim FAQs

Frequent delays and lack of communication are sometimes the first signs of a pending denial- but always a source of unending frustration. You should document every attempted contact in writing. If the silence continues, it may be time to explore legal options.

Maryland typically has a three-year statute of limitations for breach of contract, but your specific policy can have a shorter “suit against us” provision, often 12 or 24 months. The enforceability of such clauses is the subject of some satellite, or case within a case, litigation.

Yes, most standard policies exclude “groundwater” or “surface water” entering through the foundation. It’s fairly routine for an insurance company to start from the position of ‘this was a flood therefore not covered’. However, if the water entered because of a failed sump pump or a sewer backup, you may have coverage depending on your specific endorsements.

Yes, and you should. Insurance company adjusters use generalized software that may not account for the high cost of matching historic materials in Lake Evesham. A local contractor’s quote provide can essential evidence of the accurate repair cost.

Yes, the office represents both residential homeowners and commercial property owners. Anyone familiar with the area along the York Road corridor here is familiar with the flurry of economic activity traffic, raising the Specter of denied or underpaid business property claims.

Appraisal is a form of alternative dispute resolution found in some policies. If the insurer agrees there is coverage but disagrees on the amount of the loss, either party can demand an appraisal to set the value of the damage. The procedures are specific and would depend on the unique language of your insurance policy.

Any lawyer that says absolutely “no” might be to bold. Insurers perhaps generally cannot raise your rates solely because you exercised your legal right to challenge a wrongful denial- but insurance companies are free to consider all manner of factors in setting rates, renewing policies, or denying policies. Rates can be based on regional risk pools rather than individual litigation outcomes.

Why was my Evesham Park (21212) homeowners insurance claim for water damage denied?

Insurers deny water damage claims by distinguishing between sudden pipe failures and gradual seepage caused by age or deterioration. Most homeowners policies cover abrupt water events but exclude long-term leaks or maintenance-related damage. If the carrier determines the loss developed over time, it may cite policy exclusions to deny coverage.

Baltimore Insurance Lawyer Tip #56: When a carrier classifies damage as gradual, independent plumbing or forensic evaluation can help determine whether the loss was truly sudden and accidental under the policy terms.

Where is Evesham Park?

Evesham Park is a quaint, residential neighborhood located in Northern Baltimore, nestled just north of the Belvedere Square area within the 21212 ZIP code. Geographically, it is bounded by East Lake Avenue to the north, York Road to the east, and Northern Parkway to the south. This location places it within the York Road corridor, a historic artery of Baltimore that has seen significant suburban development over the last century. The neighborhood is characterized by its quiet, semi-rural atmosphere, often featuring narrow roadways with stone-lined storm gutters and an abundance of old-growth trees that provide a dense canopy throughout the summer months.

Can an insurer delay my Evesham Park 21212 claim indefinitely?

Insurers must evaluate claims in good faith but may extend review periods while conducting inspections or requesting documentation. Delays often occur when the carrier asserts an ongoing investigation into causation or coverage. Extended inactivity without explanation can raise questions about whether the delay remains reasonable under Maryland law.

Baltimore Insurance Lawyer Tip #918: A review of the claim file, correspondence, and internal notes can help determine whether a delay is supported by legitimate investigation or whether further action is warranted.

The housing stock in Evesham Park is predominantly composed of detached, single-family homes, many of which are wood-frame constructions dating back to the late 19th century through the immediate post-World War II era. The Lake Evesham Historic District encompasses much of this area, showcasing architectural styles such as Bungalows, Victorian Goths, and American Foursquares. Because many of these structures are nearly a century old, they present unique insurance challenges. The drainage patterns in the area are influenced by the natural topography of North Baltimore; while the neighborhood name might suggest a water feature, there is no actual lake, though the area is subject to moderate stormwater risks.

Flat roofs and older basements are common in Evesham Park, and these features are often focal points in insurance claim friction. The stormwater context of the 21212 area means that heavy rainfall can lead to hydrostatic pressure issues in older foundations or leaks in aging roof systems. Insurers frequently scrutinize these claims, often attempting to classify storm damage as “gradual deterioration” or “seepage” due to the age of the housing materials. Local landmarks like Belvedere Square and nearby Loyola University Maryland serve as anchors for the community, but the residential streets themselves are where the most significant insurance disputes arise. According to First Street data, properties in Evesham Park face a moderate risk of flooding, particularly from localized runoff and sewer backup during high-intensity weather events.

Why Was My Evesham Park Homeowners Insurance Claim Denied?

- Policy Exclusions: Many policies contain specific language that excludes certain types of damage, such as floods, earth movement, or specific “named perils” that were not purchased as part of the coverage.

- Lack of Proper Maintenance: Insurers often claim that the damage was not caused by a sudden event but was instead the result of long-term neglect, wear and tear, or failure to perform necessary repairs.

- Late or Incomplete Filing: Failing to notify the insurance company within the timeframe required by the policy, or failing to provide a complete “Proof of Loss” statement, can lead to an automatic denial.

- Disputed Cause of Loss: The insurance company may argue that the primary cause of the damage was an excluded event (like a slow leak) rather than a covered one (like a sudden pipe burst).

- Misrepresentation or Fraud Accusations: If an insurer believes that the policyholder provided inaccurate information during the application process or when filing the claim, they may deny coverage entirely.

| Local Factor | Why This Matters for Insurance |

|---|---|

| Historical Housing Age | Older materials (lath and plaster, frame construction) are often cited as pre-existing conditions in storm damage denials. |

| Stormwater Runoff Patterns | Localized drainage issues in the 21212 zip code can lead to basement seepage, which insurers frequently exclude as “surface water.” |

| Flat Roof Prevalence | Insurers often apply a lower “actual cash value” or deny claims entirely if a flat roof is deemed past its useful life. |

ate investigation or whether further action is warranted.

Homeownership Evesham Park 21212

The residential landscape of Evesham Park 21212 is a study in architectural longevity and community stability. With an average home age exceeding 80 years, many residences require specialized maintenance to withstand the shifting climate patterns of the Mid-Atlantic. According to Live Baltimore, the neighborhood features a high ratio of owner-occupancy, which traditionally correlates with higher levels of property care; however, the age of the housing typology—predominantly frame cottages and bungalows—leaves them susceptible to specific storm exposure patterns. In North Baltimore, the prevalence of flat roofs on older additions and the use of stone-lined gutters can create maintenance-related denial risks when gutters clog or older roof membranes fail during high-wind events.

Civic engagement is high through groups like the Lake Evesham Community Association, which advocates for local infrastructure improvements and historical preservation. While the neighborhood is not situated in a high-risk tidal flood zone, its riverine and localized drainage risks are significant due to the Baltimore City Floodplain management regulations that oversee the 21212 area. Property owners often face friction when insurers cite “sewer backup” as the cause of basement flooding—a peril that may be excluded if the homeowner did not specifically add an endorsement for it. Hyperlocal building conditions, such as aging terra cotta pipes and unlined chimneys, further complicate the “wear and tear” arguments used by adjusters from national carriers.

Evesham Park (21212) Housing & Economic Snapshot

| Metric | Value | Source |

|---|---|---|

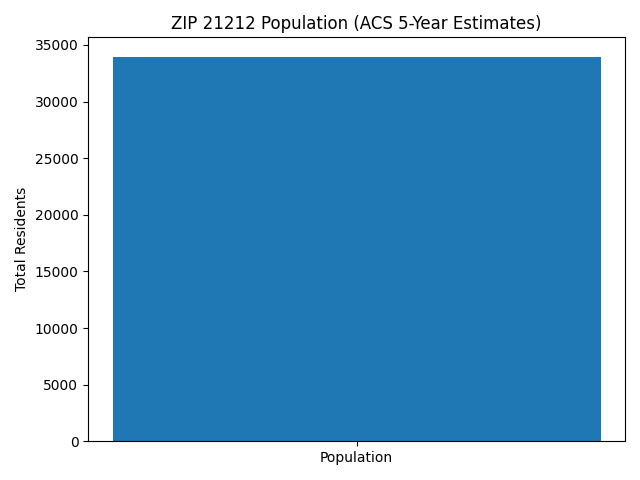

| Population | 33,974 | American Community Survey (2024 5-Year Estimate) |

| Owner-Occupied Housing | 68.8% | ACS 2018-2022 5-Year Estimate |

| Renter-Occupied Housing | 31.2% | ACS 2018-2022 5-Year Estimate |

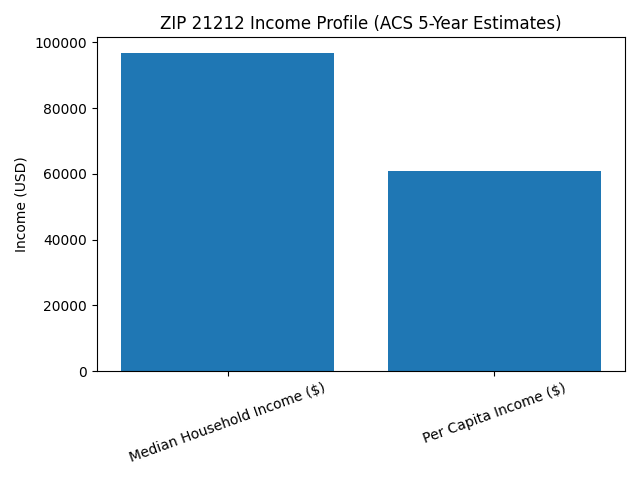

| Median Household Income | $96,685 | ACS 2024 5-Year Estimate |

| Per Capita Income | $60,998 | ACS 2024 5-Year Estimate |

How do I dispute an underpayment from my insurer?

Homeowners dispute underpayments by comparing the insurer’s repair estimate with independent contractor assessments. Differences in scope, pricing methodology, or depreciation often explain payment gaps. Clear documentation and localized cost analysis in Evesham Park 21212 can clarify whether the issued amount reflects covered damage.

Baltimore Insurance Lawyer Tip #675: Thorough documentation, updated estimates, and a structured comparison of repair methodologies can strengthen a challenge to an underpaid claim.

How to Challenge a Evesham Park Insurance Claim Denial — My Steps:

When I take on a case in Evesham Park, I apply a diligent, experienced, and aggressive approach to ensure the insurer meets its contractual obligations.

Policy Analysis The first step is a comprehensive review of the entire insurance contract. I look for internal contradictions in the exclusion sections that may allow for coverage where the insurer claimed none existed.

Evidence Building I work with engineers, plumbers, or other professionals to document the true cause of loss. In Evesham Park, this can mean proving that a roof failure was caused by e.g. a specific wind event rather than long-term deterioration.

Litigation Filing If the insurer refuses to move from their denial, I file a formal lawsuit in the Baltimore City Circuit Court. This shifts the dynamic, forcing the carrier to defend their decision under the scrutiny of Maryland’s legal standards.

Discovery During this phase, I demand the insurer’s internal claim file. This often reveals the “instructions” given to the field adjuster and whether the company ignored evidence that favored the homeowner.

Trial Preparation I prepare every case as if it is going to a jury. By showing the insurer that we are ready for trial, we create the necessary leverage to secure a fair settlement or a court award.

Does a flat roof in Evesham Park 21212 affect my insurance claim?

Flat or low-slope roofs often receive heightened scrutiny from insurers due to drainage concerns and wear patterns. After a storm event, disputes typically focus on whether damage resulted from wind or hail, which is usually covered, or from age-related deterioration, which is commonly excluded.

Baltimore Insurance Lawyer Tip #675: Engineering or roofing assessments can help determine whether a specific storm event was the primary cause of the damage rather than gradual wear.

Next Steps After a Denial

- Stabilize and Preserve the Scene of the Loss: Take immediate steps to prevent further damage, such as tarping a roof or board-up services. Do not make permanent repairs until the insurer has completed their inspection.

- Mitigate Further Loss: You have a duty under your policy to prevent additional damage. Keep receipts for all temporary repair costs.

- Notify Your Insurance Company Immediately: Ensure all communication is documented. If you have already received a denial, request the specific policy language they are relying upon in writing.

- Comply with Policy Conditions & Your Duty to Cooperate: Provide the requested documents and allow access for inspections, but keep a log of everything provided.

- Keep Your Denial Communications: Save every letter, email, and voicemail from your adjuster. These are vital pieces of evidence in a breach of contract case.

- Seek Legal Guidance: Contact Eric T. Kirk to discuss the mechanics of your denial and determine if the insurer has violated the terms of your policy.

Insurance Portals:

Your Chosen Insurance Chose Not to Pay You. Choose Me.

So Should You.

Nearby Neighborhoods

- Lake Walker Insurance Claim Denial Lawyer

- Cedarcroft Insurance Claim Denial Lawyer

- Belvedere Insurance Claim Denial Lawyer

Injured in a Evesham Park car accident? Learn about your rights here.