Outlining Denied Insurance Claims for Baltimore’s Midtown | 21201

TL;DR (Midtown 21201 — Denied Insurance Claims)

- Midtown residents often face lowballing, stonewalling, and exclusions in homeowners’ and property-damage claims.

- Insurance carriers routinely deny coverage based on policy exclusions, “maintenance,” delayed notice, or disputed cause of loss—often incorrectly.

- You owe the insurer cooperation, but you do not have to accept an improper denial.

- A seasoned Baltimore insurance claim denial lawyer can challenge policy-based refusals, engineer reports, and damage-cause disputes.

- Midtown 21201 homeowners: Speak plainly—if your insurance carrier is jerking you around, get counsel immediately.

Midtown’s densely packed housing stock—rowhomes, subdivided properties, small commercial conversions—means a lot of claims trace to:

- Wind + hail

- Pipe bursts + water infiltration

- Stormwater intrusion

- HVAC failures

- Basement water

- Electrical fire

- Landlord/tenant-caused loss

And here’s the rub:

Insurers often try to reclassify the cause into something not covered.

I see this daily.

“Freezing? No, that’s ‘poor maintenance.’”

“Wind? No, that’s ‘wear and tear.’”

They twist the language. My job is to untwist it.

Why Was My Midtown Homeowners Insurance Claim Denied?

Common Reasons for Midtown Homeowners Insurance Claim Denials.

- “Policy Exclusions: Insurers often deny claims by citing exclusions in the policy, such as flood, freezing, earthquake, or mold damage. However, these denials can sometimes be challenged depending on policy wording and state law. Every successful challenge to a denied claim starts with an analysis of the insuring agreement.

- Lack of Proper Maintenance: Insurance companies may argue that damage resulted from homeowner neglect rather than a covered peril, placing the financial burden on you. Insurance policies issued in Baltimore typically do not cover “wear and tear”.

- Late or Incomplete Filing: Failing to notify the insurer promptly or not providing the required documentation can be used as a reason for denial. Every successful challenge to a denied claim necessarily includes the insured person cooperating fully with their insurance company.

- Disputed Cause of Loss: Insurance adjusters may claim that the damage was caused by a non-covered event, even if the evidence suggests otherwise. This bewilders homeowners, frustrates Baltimore’s homeowners, and often has to be litigated in Baltimore’s courtrooms.

- Misrepresentation or Fraud Accusations: If an insurer suspects inaccurate information was provided—whether intentional or not—they may use it as grounds to deny a claim. I do not handle fraudulent claims. If you have been unfairly or unjustly accused of fraud, I will help you. If your claim has been denied for any of these reasons, or any other reason, it is critical to have an experienced Baltimore insurance claim attorney review your case. Insurers often rely on technicalities to avoid paying rightful claims. A strong legal advocate can challenge their tactics.”

Nearby Neighborhoods: Canton Roland Park Hampden

FAQ- Denied Insurance Claims in Midtown 21201

Why do insurance companies deny claims in Midtown?

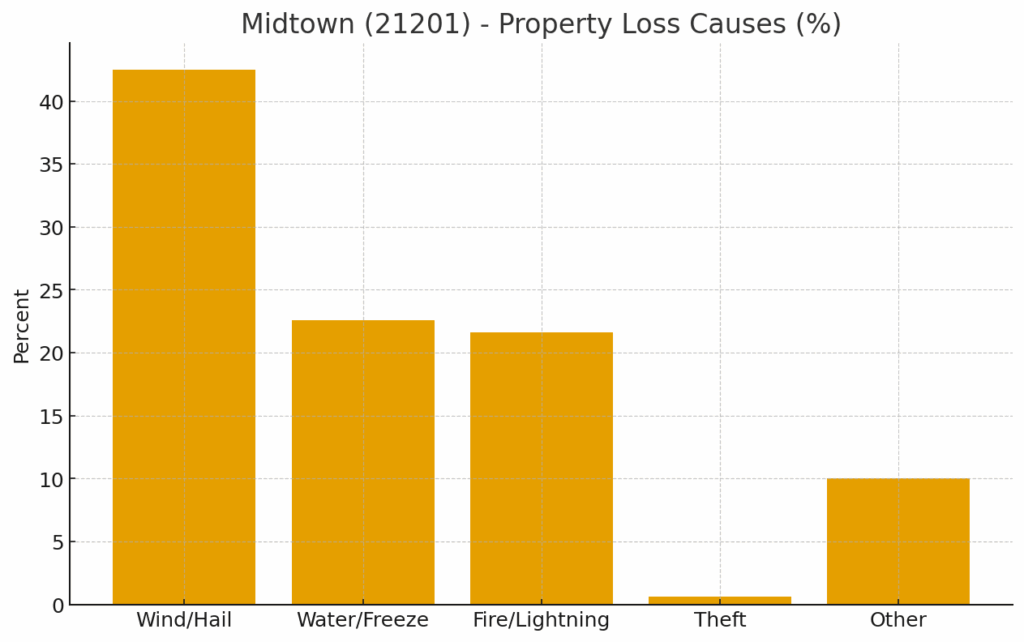

There are no statistics that I am aware of that break down claim denial rationales at a granular level. Claims arise in Midtown. Experience tells us that claims are denied and undervalued here. The Insurance Information Institute tells us the perils reported in call claims in 2023 were:

Wind and hail 42.5

Water damage and freezing 22.6

Fire and lightning 21.6

Theft 0.6

All other property damage 10.0

Liability 2.1

Credit card and other 0.6

The answer is always immediately, even though the statute of limitations is 3 years.

Read the Law: Article – Courts and Judicial Proceedings 5-101

Midtown Insurance Lawyers Tip 82: An insurance company, who invariably benefits from delay, will always blame delay on you.

When an insurance company denies a claim, they have to give you a reason, in writing. Their reason is subject to challenge. I can help you win that challenge.

Midtown Insurance Law 101: The insurance company has to justify the stated reason for the denial.

You can “file” a complaint with me. If I can help, I will file a legal document actually called a “complaint” that starts a lawsuit.

Additional Midtown Insurance Resources:

Maryland Insurance Administration

Initially, unfortunately, your insurance company does. Ultimately, a judge or juror is the ultimate arbiter of whether a covered loss occurred.

Midtown Insurance Lawyers Tip #6: In some instance “coverage” issues may be determined by a judge at the summary judgment stage.

Read the Law: Rule 2-501. Motion for summary judgment.

Time needed: 365 days

How To Overcome Denied Insurance Claims in Midtown

- How to request your insurer’s claim file

This might be in the realm of trick questions. You can ask. They will likely give you the portions of the file they want you to see.

Midtown Insurance Lawyer’s Tip #456: Once suit is filed, you can invoke the discovery powers to the court to get documents, and have questions answered.

Midtown Insurance Lawyer’s Tip #457: Even then, they will fight and claw not to give it to you. - How to request an adjuster reinspection

This is not a trick question. You ask. You should be able to prove you asked.

Midtown Insurance Law 101: The insurance company is not obligated to give you a more favorable assessment, opinion or offer, just because they “looked again” - How to obtain an independent contractor estimate

Other than hiring an experienced Midtown insurance claim denial lawyer, this is likely the most important choice you face. It is unlawful to act as a home improvement contractor or salesperson without a license. The Maryland Home Improvement Commission (MHIC) 410.230.6309 can verify, or, you can:

Northwood Home Improvement Contractor Verification. - How to determine whether flood exclusions apply?

The same process applies here as with any other coverage issue. You must start with the policy.

Midtown Insurance Lawyer’s Tip #809: The legal analysis is to determine what the coverage under the policy is, and, then, if the insurer an prove an exclusions apply.

Next Steps After a Midtown Homeowners Insurance Claim Denial

Eric T. Kirk

Midtown Homeowners Insurance Claim Denial Litigator- Stabilize and Preserve the Scene of the Loss • If your home has been damaged, take immediate action to prevent further harm. • Avoid making permanent repairs before your claim is fully evaluated, but you must take steps to prevent worsening conditions. The classic example,- known to Floridians who have had their hurricane damage claims denied by the nation’s largest insurance companies- as covering a leaking roof with a giant blue tarp). • Take photos and videos to document the damage as soon as possible.

- Mitigate Further Loss • Baltimore’s homeowner’s policies likely include a duty to mitigate loss, meaning you must take reasonable steps to prevent additional damage. Even if it does not contain that clause, substantive law requires the homeowner to employ measures to stop additional loss or damage. This is the Duty to Mitigate. • This could include shutting off water in the event of a plumbing failure or securing broken windows.

- Notify Your Insurance Company Immediately • Contact your insurance company to formally report the loss. Do this in writing whenever possible to create a record of your communication. Use a portal if one is available, but retain screenshots, and independent records.

• State Farm — https://www.statefarm.com/claims

• Traveler’s — https://www.travelers.com/claims

• Allstate — https://www.allstate.com/claims/file-track

• Nationwide — https://www.nationwide.com/insurance-claims/

• USAA — https://www.usaa.com/ - Comply with Policy Conditions & Your Duty to Cooperate • Insurance policies often have strict duties after a loss, such as providing a sworn proof of loss, giving recorded statements, or attending an examination under oath. • Failing to comply can give your insurer additional grounds to deny your claim. The courts in Baltimore have found that a homeowner’s refusal to adhere to these contract obligations can bar the insurance claim forever.

- Keep Your Denial Communications • Your insurance company is required to give a written for your claim denial. Retain this document, with all others. Once your claim is denied, your legal rights are locked in, but, the clock starts ticking. Statute of limitations. • Keep all correspondence, including emails and letters, in a dedicated file. The Denial of your insurance claim in a vital juncture in the process of you being made whole for your loss. It is when your claim has been denied, in whole or in part, that I can likely be of the most assistance.

- Seek Legal Guidance from an Experienced Baltimore Insurance Claims Denial Attorney • Do not accept the denial at face value—Not all insurance claim denials are misplaced. Insurance companies sometimes deny valid claims for reasons that may be challenged in court. What do you do when your insurance company is in denial? • An experienced Baltimore insurance claims attorney will review your policy, analyze the insurer’s reasoning as contained in their denial letter, and litigate on our behalf to overturn an unfair denial.

Eric T. Kirk has spent a career holding insurance companies accountable for wrongfully denied claims. When you hire our firm, we will: ✔ Complimentary Case Analysis – Fight Back Against Unfair Denials ✔ Analyze your policy and determine whether the insurer’s denial is valid. Every successful challenge to a denied claim starts with an analysis of the insuring agreement. ✔ Gather your evidence to support your claim. Most edmondson village denied insurance claims require expert analysis on the cause of loss and nature of damage. ✔ Negotiate aggressively and consistently with your insurer, seeking to engineer a fair settlement. If not ✔ File a lawsuit I sue insurance companies ✔ Take your case to trial. I try cases against insurance companies.

“I can tell you the nation’s largest insurance companies hire very skilled, very talented, very aggressive lawyers to take their cases to trial.”

SO SHOULD YOU.

In Summary

Midtown residents frequently face insurance denials after water, storm, or structural damage. Insurers often rely on exclusions and technical limitations to avoid payment. An experienced Baltimore denied insurance claim lawyer helps challenge denials, evaluate policy language, and pursue owed benefits.

Contact Eric T. Kirk for a free consultation.